A Most Hawkish Hike by the ECB

Thursday’s ECB (European Central Bank) rate hike and its confirmation of a faster balance sheet reduction were in line with most investors’ expectations. But its projections and its policy statement suggested a notably more hawkish policy outlook. The ECB downgraded its projections for GDP growth – but just a touch, considering how much weaker recent data has been. More importantly, it raised its outlook for inflation in every year of its forecast. That includes 2025, for which the ECB now sees inflation at 2.2%, still above its target. All this suggests that the ECB is prepared to take its main policy rate from 3.50% to close to 4% against a backdrop of weakening consumption, which remains below its pre-pandemic level. For now, though, it looks like the ECB’s key variable is real-time inflation data.

Our Take on the Meeting

The ECB delivered a further 25 bps rate hike, as investors had expected. Alongside this hike, it confirmed that it would reduce its balance sheet more quickly than previously announced. So far, so predictable. But President Lagarde’s decidedly more hawkish tone was a surprise. Her press conference made clear that the ECB is determined to differentiate its policy plans from the Fed’s hawkish skip earlier this week (Will the Fed’s Policy Bundle Bundle Morph into a Bungle?). The question is why. In its updated economic projections, the Bank downgraded its GDP growth outlook ― but just a touch, considering the weaker data flow. More surprisingly, it raised its inflation outlook in every year of its forecast. That includes 2025 (the final year of its projections) for which the ECB now sees inflation at an average 2.2%, still above its target. President Lagarde attributed this miss to high unit labor costs that are expected to persist. But when probed, she conceded that, although the eurozone labor market is strong, there are no signs of a wage-price spiral. Our take is that the ECB has incorporated the risk that a wage-price spiral will crystallize into its forecast and that this underpins its more hawkish stance. This suggests that it is on track to take its main policy rate to close to 4%, even if domestic demand is weakening, with consumption still below its pre-pandemic level. As a result, our view is that the ECB will hike rates a further 25 bps at its next meeting, before pausing as economic activity continues to deteriorate in the second half of 2023. This view reflects our forecast that GDP growth will fall from 0.6% (market consensus) in 2023 to 0.4% (below market consensus) in 2024.Market Reaction

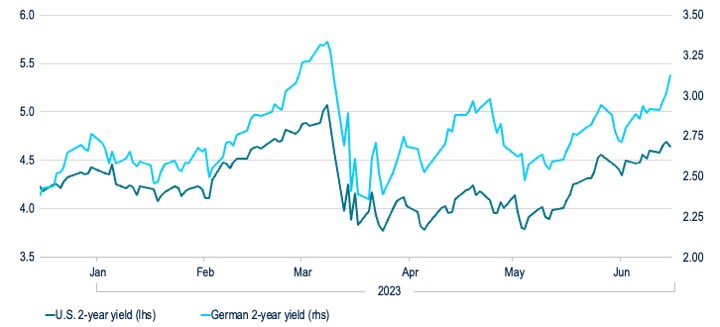

The ECB’s decision on interest rates and on its balance sheet was as investors expected. But the Bank’s inflation projections and its press conference were a hawkish surprise. Comparisons with the Fed’s decision one day earlier are hard to avoid: if the Fed's decision was a hawkish skip, the ECB’s was a most hawkish hike. Thursday’s market reaction reflected that hawkish message. German Bund yields rose sharply, with rising short-dated yields further flattening the German yield curve. Short-term government bond markets moved quickly to price in more than a 25 bps ECB rate hike in July and close to another 25 bps in September. Risk assets were generally resilient after the ECB’s rate hike. That resilience was remarkable, given that the Bank’s hawkish message comes as the eurozone economy is still weakening. Italian and Spanish spreads over German yields for example, remained broadly stable. After an initial spike, credit spreads widened only marginally on the day. The most prominent move, perhaps, was in the currency market, where the euro appreciated sharply relative to the U.S. dollar. Its surge, despite the threat of weaker eurozone growth, reflected interest-rate differentials that moved sharply in favor of the single currency. Investors have been surprised recently, as developed-market central banks refuse to pause but continue to fight inflation. The ECB is in a league of its own as it continues to signal further tightening, with no hint of a pause. Its stance raises a significant concern for European risk assets, because further tightening would coincide with a weakening economy that is vulnerable to further supply shocks. Together with higher interest rates across the yield curve, this confirms our view that risk assets (including corporate bond spreads) in the eurozone are vulnerable.Figure 1: German 2-year Bund yields have risen sharply, relative to 2-y U.S. Treasury yields, following the ECB decision (yields in %).

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in