PGIM Fixed Income

-

Italy's Bank Tax: It's Hard to Please Everyone All of the Time

The Italian government’s unexpected announcement earlier this month of a 40% one-off tax on local banks’ domestic excess profits prompted a negative market reaction. Although the selloff was enough for Italy’s finance ministry to scale back the tax the next day, the muddled episode provides another reminder of how heightened political polarization can impact investors.1 In its wake, the situation raises doubts in investors’ minds about the Italian government’s market friendliness and about Italian banks’ vulnerability to future political meddling.

An Unexpected Surprise…

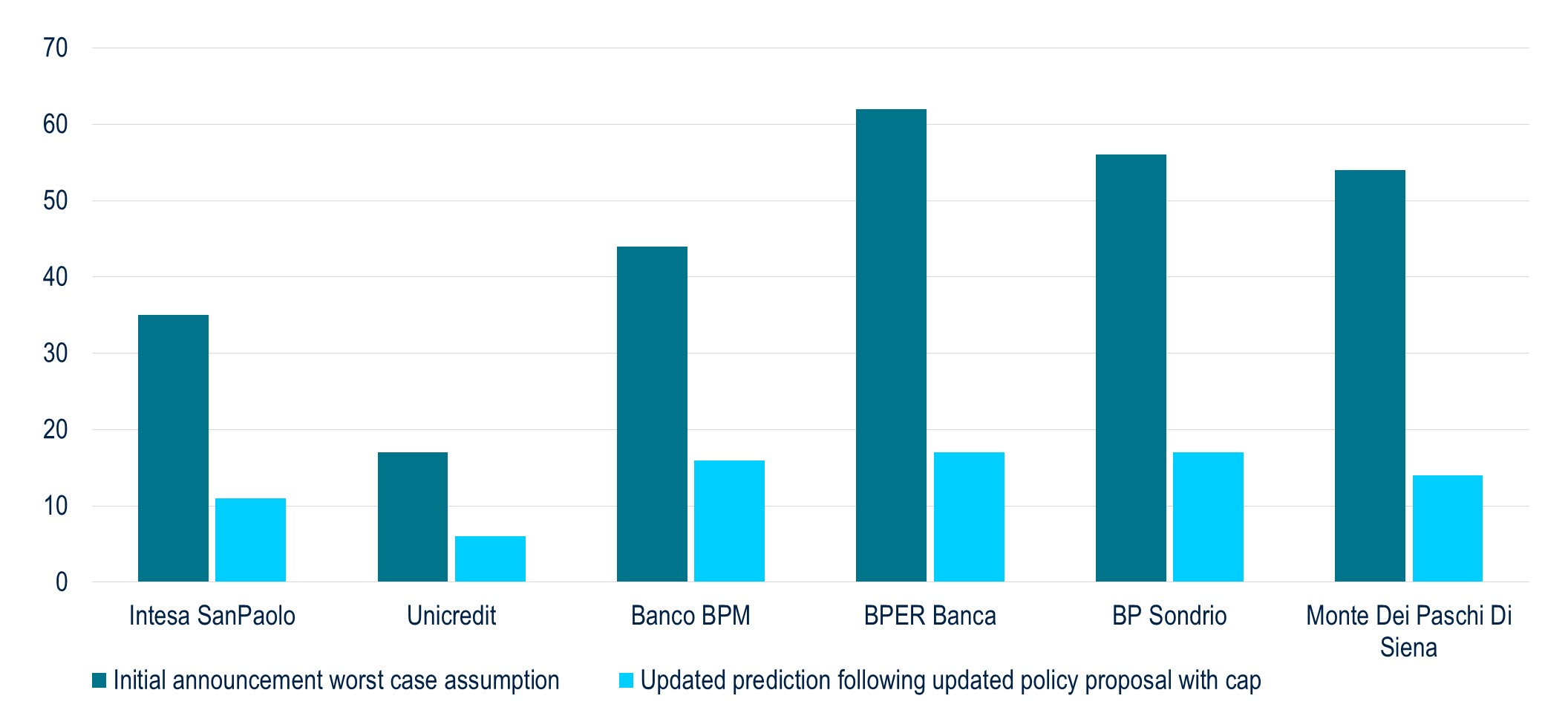

Italian banks are doing well. We expect the two leading Italian banks’ domestic net interest income, the largest component of their profits, to grow 79% in 2023, compared to 2021. As a result, however, politicians and customers have accused the banks of excessively profiting from rising ECB rates and of passing on too little of those increases to savers. Nevertheless, this month’s windfall tax surprised banks and investors. Deputy Prime Minister Salvini announced it in a speech on August 7, without the finance minister present and with little detail on how the government would calculate the tax. Italian bank spreads underperformed, and investors’ initial reaction wiped over €10 billion off Italian banks’ combined market cap. This loss far exceeded the €2-€3 billion that the government hoped to raise. So, one day after it announced the bank tax, the government hastily capped it at 0.1% of each bank’s assets. After the cap, the impact on Italy’s banks would be less than half what investors initially feared (Figure 1), and share prices recovered around 60% of the initial selloff.Figure 1: Italy’s larger banks should weather the revised tax better than their smaller peers. (impact of bank levy as % of predicted 2024 group net income)

Image

…More Damaging Than Necessary

Our estimate of the sector-wide impact of the revised tax now lines up with the €2-€3 billion that the government was aiming for. This is a number that Italy’s banking sector can easily absorb. The country’s big banks, in particular, are set for record profits this year—admittedly, after years of poor performance—and have been returning capital to shareholders. For the largest domestic banks, Intesa Sanpaolo and Unicredit, we calculate hits of 11% and 6% of expected 2024 net income, respectively (the tax only applies to domestic operations, so Unicredit fares better because it is more internationally diversified). Smaller banks, with generally poorer profitability and less efficient balance sheets, see a proportionally larger hit. But even for them, this tax is a minor setback as their credit profiles have improved in recent years. Windfall taxes aren’t unique to Italy, and they don’t have to elicit market routs. Spain’s bank tax, introduced in July 2022, led to a similarly negative initial reaction. But Spanish banks did not see a permanent risk premium, partly because their underlying earnings continued to improve, which outweighed the tax. Italy’s tax, on the other hand, comes as banks’ margins look to be at cyclical highs, as the ECB rate cycle peaks. Moreover, the nature of Italy’s surprise announcements, with few details and poor communication, disquieted investors. Prime Minister Meloni belatedly took “full responsibility” and said that she stands behind the tax. She has worked to portray herself as business-friendly but has damaged those ambitions with this measure. Italy’s parliament is yet to approve the tax and could alter it again, as even some of Meloni’s own government coalition support scaling it back. This tax reminds investors that banks’ performance can depend on politics as much as on financial fundamentals. As a result, the latest episode may complicate one of the government’s other aims, to sell its stake in bailed-out bank Monte dei Paschi di Siena.A Broader View: Macroeconomics and Italy’s Fiscal Policy

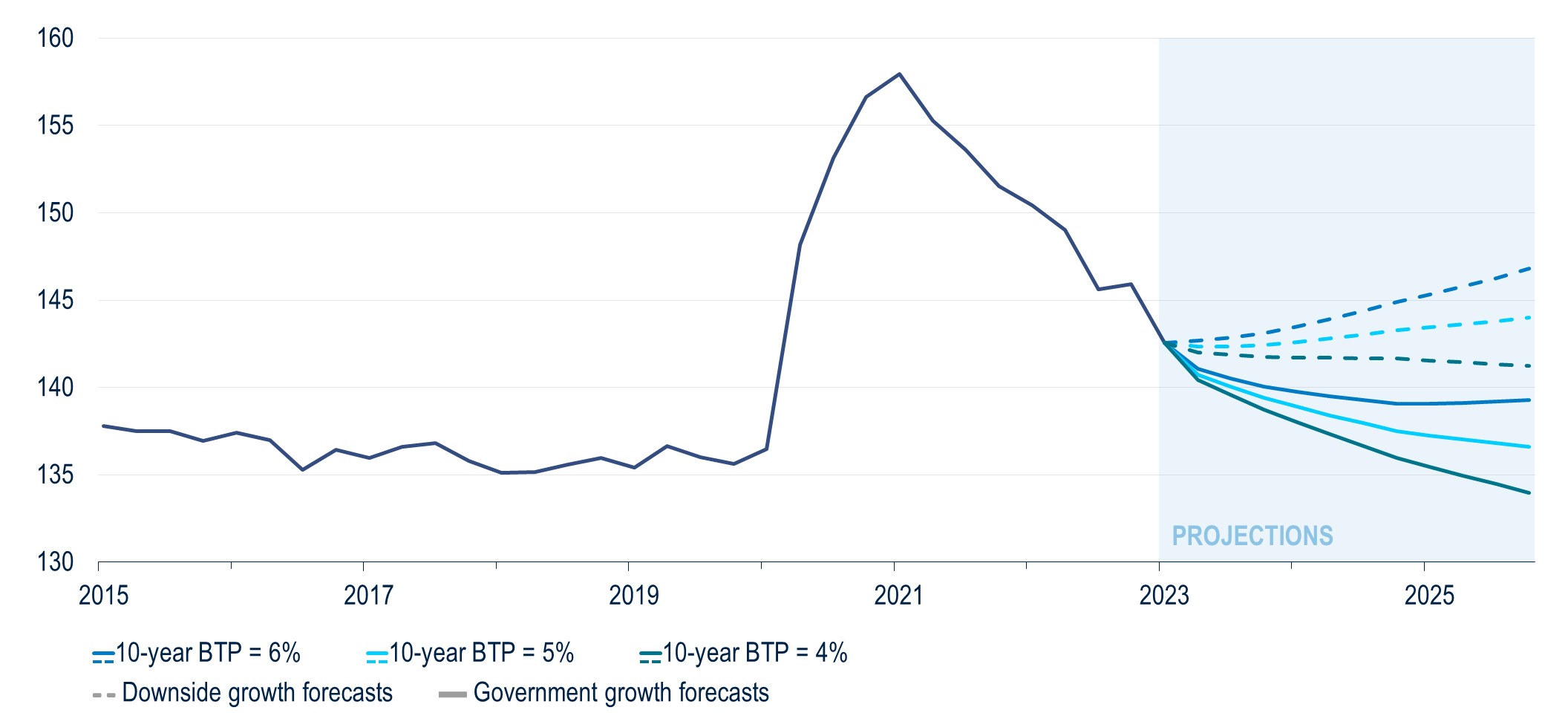

Last year, we expressed our near-term confidence in Italy’s political, economic, and fiscal outlook (Italy: Europe’s “Sleeping Beauty”). At the time, we did not think that the ECB's impending rate hikes would lead to significantly wider Italian bond spreads. That earlier view has aged well. Our analysis last year suggested that a decline in Italy’s debt-to-GDP ratio was all but certain, and that high nominal GDP growth would more than offset the effect of rising interest rates. Since then, upside surprises to inflation have lowered Italy’s debt-to-GDP ratio even more rapidly than we had expected. Figure 2 shows that, if the yield on Italy’s 10-year sovereign bond (BTP) stays around today’s levels of 4%, the country needs annual nominal GDP growth of at least 2.5% to bring down the debt-to-GDP ratio.Figure 2: The reduction in Italy’s debt-to-GDP ratio may be short-lived. (Italy debt-to-GDP ratio, %)

Image

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in