The Fed's Higher-for-Longer Mantra is OK for Bonds

The Federal Reserve went to great lengths to indicate that policy rates will likely remain elevated for some time and that neutral policy may indeed be higher than previously projected. While higher rates are still possible, yield levels are back to historically attractive levels that point to productive conditions ahead. “Higher for longer.” That was the message Fed Chair Powell wanted to make clear—and it was everywhere today. The removal of two cuts from the 2024 dots combined with a growth profile that is now stronger (not just this year, but next year as well)—with unemployment rate forecasts that are also much improved—drives the mantra home. Of course, higher doesn’t necessarily mean more hikes from here. Yes, the median dot still sees another hike (12 of 18 members see an additional increase). And Powell did the right thing by keeping the door open to that possibility (as we said after the last FOMC meeting, central bankers relish optionality). But throughout the press conference, Powell never leaned in the direction of believing the median estimate would necessarily be realized. In fact, we think he did a great job of striking a balance between another hike or being done—our own view remains that the hiking cycle is over. It was also noteworthy that in today’s unveiling of the 2026 dots, the Committee still does not have Fed funds hitting the long-run average (which was unchanged at 2.5%). We think this serves two purposes. First, it is yet another way of driving home the higher-for-longer mantra, and second, that a level above 2.5% is the direction of travel for the long-run dot. It’s going higher, and it’s just a question of when at this point. In fact, as we looked through the 2026 forecast stack, there was some movement higher in the dots. The top five dots in that stack shifted up, where the prior average was 3.075% and now it sits at 3.45%. So, the hawks became more hawkish. The only other change that caught our attention was an alteration to the Statement. The current labor market assessment was downgraded somewhat. The Fed had characterized it as “robust,” but they now say it “slowed” and were quick to add that “it remains strong.” That last bit reduces the drag from the wording downgrade, but clearly it became harder to ignore the slowing that is underway. We think continued slowing is ultimately what will get the Fed to realize the cuts that it penciled in for next year.

A Yield Flashback and its Implications

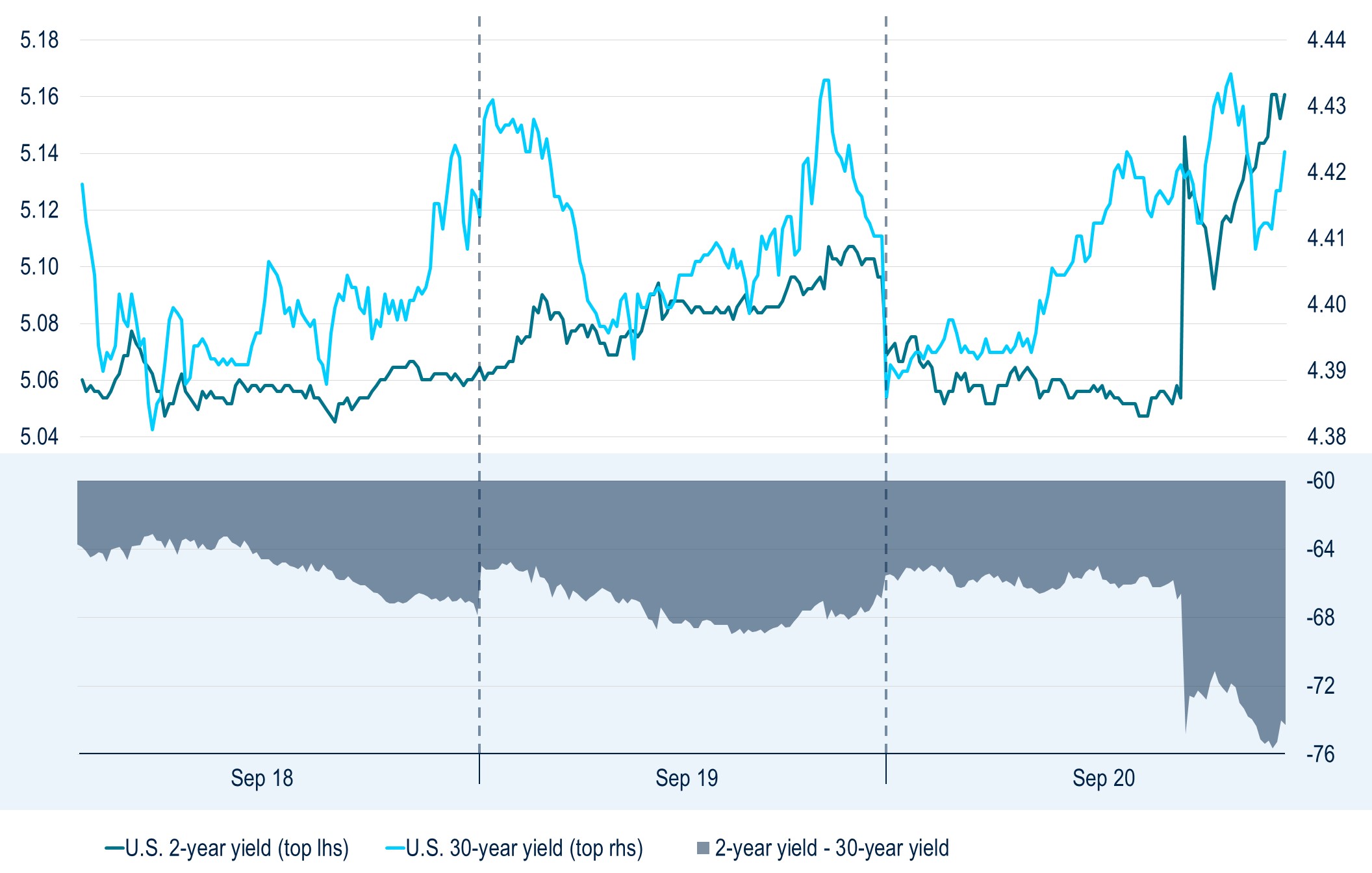

The Fed’s vigilance against inflation pushed the 2yr/30yr Treasury yield curve another 8 bps deeper into inversion driven by a 10 bp+ move higher in the 2-year yield (Figure 1). After rallying intra-day, the 30-year Treasury ended up nearly unchanged. Risk markets ended weaker on net, with credit spreads widening and stocks falling.Figure 1: The back of the Treasury yield curve indicates confidence in the Fed’s ability to contain inflation over the long term (%).

Figure 2: The last few months reinforce that a hawkish Fed is more of a risk for equities than corporate bonds (LHS: index level; RHS: bps).

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in