The Limited Impact of the U.S. Downgrade on Munis

Fitch Ratings recently became the second of the three major ratings agencies to downgrade the U.S. long-term debt rating to AA+, below the AAA rating currently assigned to twelve U.S. states.1 While somewhat counterintuitive, this relationship is not surprising. U.S. states benefit from numerous structural strengths and constraints that encourage a fiscal discipline consistent with credit ratings higher than that of the sovereign. While states are impacted by the policies and performance of the U.S. government, the credit quality of states as a group is not constrained by the U.S. sovereign rating and we don’t expect the U.S. downgrade to have an outsized impact on muni bond valuations going forward. Ultimately, state credit quality hinges on each state’s ability to allocate resources to meet demands which are limited only by the constraints of its own economic environment and governance framework. As such, credit quality varies across states, and is not directly dependent on the sovereign rating of the U.S. U.S. states benefit from structural advantages that collectively provide sufficient autonomy to allow for higher ratings than the U.S. sovereign. First, states’ autonomy to manage their obligations is nearly unlimited. A state’s ability to impair a contract has been upheld by the U.S. Supreme Court (US Trust v New Jersey 1974, Home Building & Loan v Blaisdell 1974) provided it can show it is reasonable and necessary to do so. Further, states enjoy a high degree of operating flexibility, given their unlimited taxing power and broad, diverse tax bases. States also have substantial autonomy over the spending side of the budget. For example, while not always politically easy, states have the authority to reduce or delay aid to local governments during periods of economic weakness.

Fiscal Discipline

While states enjoy substantial autonomy, they do face certain constraints which encourage fiscal discipline. Most notably, states are bound by their constitutions to balance their budgets. This requirement varies by state in terms of stringency. For example, there is substantial variation in terms of how revenues are estimated and the process by which the budget is approved. Further, states have varying requirements related to the maintenance of budget balances throughout the fiscal year, largely related to the power of the governor to impose mid-year budget adjustments. Nevertheless, state balanced budget requirements provide a baseline level of fiscal accountability. States’ ongoing need to access the capital markets also creates a strong incentive for debt repayment. While the generally high credit quality of states reflects the structural strengths of the sector, in certain instances credit quality is enhanced by constitutional or statutory provisions that insulate debt repayment from any ongoing operating stress. For example, California’s constitutional payment prioritization system and Illinois’ statutory debt repayment mechanics strengthen the security pledge behind those states’ GO bonds. Unlike other sub-sovereign issuers (e.g., Canadian provinces), U.S. states borrow primarily to fund capital investment. As they are not reliant on capital markets for debt repayment, states retain flexibility to optimize the timing of bond issuances.Federal Support

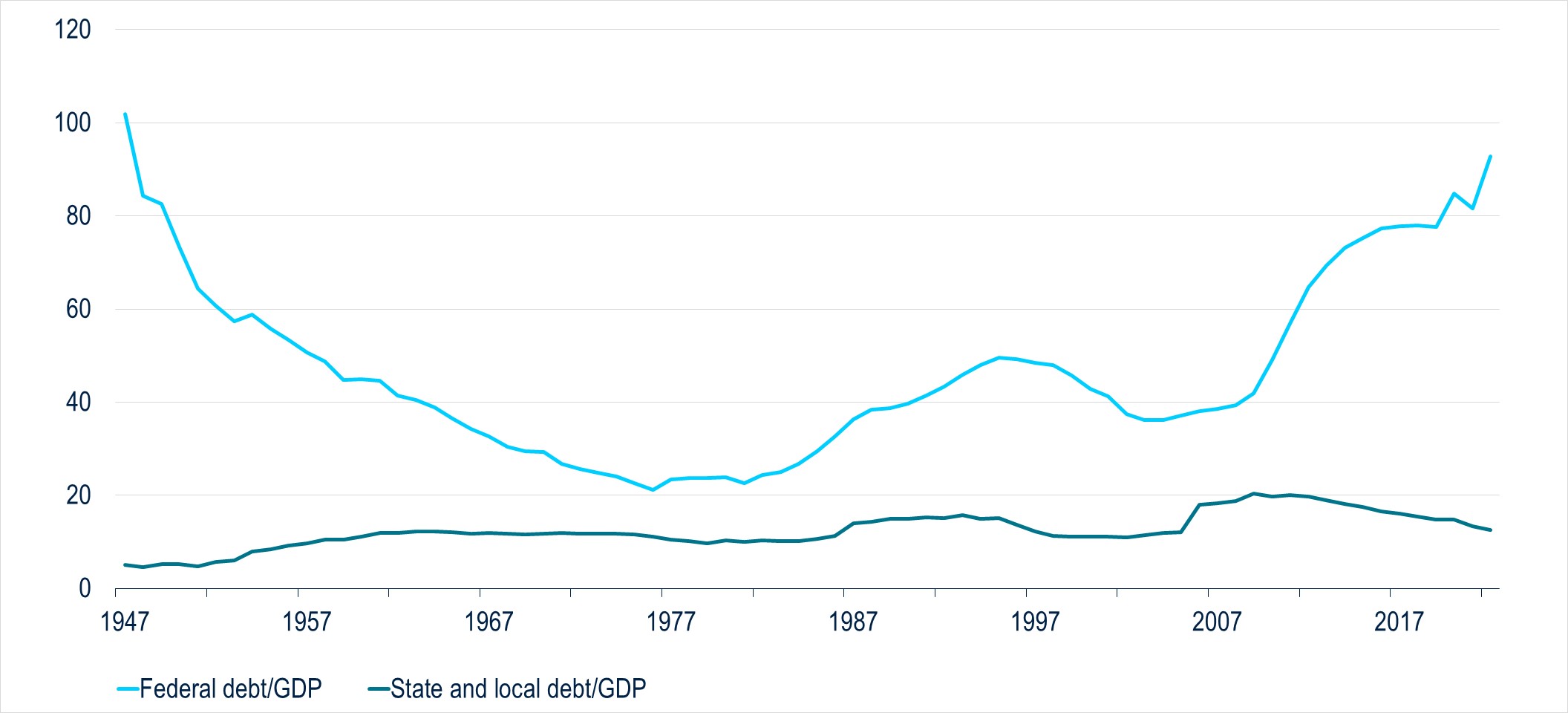

In addition, states benefit from the U.S.’s macroeconomic and structural strengths. These include the nation’s strong rule of law and respect for property rights, which underpins bondholder security, as well as the nation’s sound and well-regulated banking and financial systems. While we do not assume the federal government will backstop state operations or debt payments, states have historically benefited from federal aid (FEMA) following natural disasters or events such as the 9/11 attacks. At the same time, states are required to fund fewer services than the U.S. government, leading to lower debt-to-GDP (Figure 1). For example, the federal government must fund defense, social security and Medicare, in addition to a substantial share of safety net services (including Medicaid) in partnership with states and local governments.Figure 1: Federal versus State and Local Debt to GDP (%)

Federal Impacts on State Credit

Despite their inherent strength and sovereign status, state credit quality may be impacted both directly and indirectly by federal policies, and these impacts are factored into our state credit ratings. For example, states have little control over the amount of federal funding they receive and are subject to federal spending mandates. Most notably, proposals that would alter the federal funding of Medicaid, a shared state-federal program, could have significant and direct implications for state budgets. State economic trajectories are also directly affected by federal policies and priorities, as we see in the impacts of the allocation of COVID-19 stimulus funding or in the imposition of the SALT deduction cap. Finally, states with relatively high exposure to federal employment and/or procurement are indirectly vulnerable to budget cuts during periods of federal fiscal consolidation. In these ways, individual states may be impacted, either positively or negatively, by the actions of the federal government. The potential for federal government dysfunction to impede state credit quality is notably reflected in our ratings for Grant Anticipation Revenue Vehicle (GARVEE) bonds, which are secured by grants of federal transportation funds and typically have maturities that extend beyond current federal highway funding authorizations. Absent a backup pledge of state revenues, timely congressional action is necessary to maintain the flow of pledged funds for these bonds. Ratings on GARVEE bonds tend to be materially lower than state ratings (generally in the A category in the absence of an additional state revenue pledge), to account for this reauthorization risk.Limited Impact on Valuations

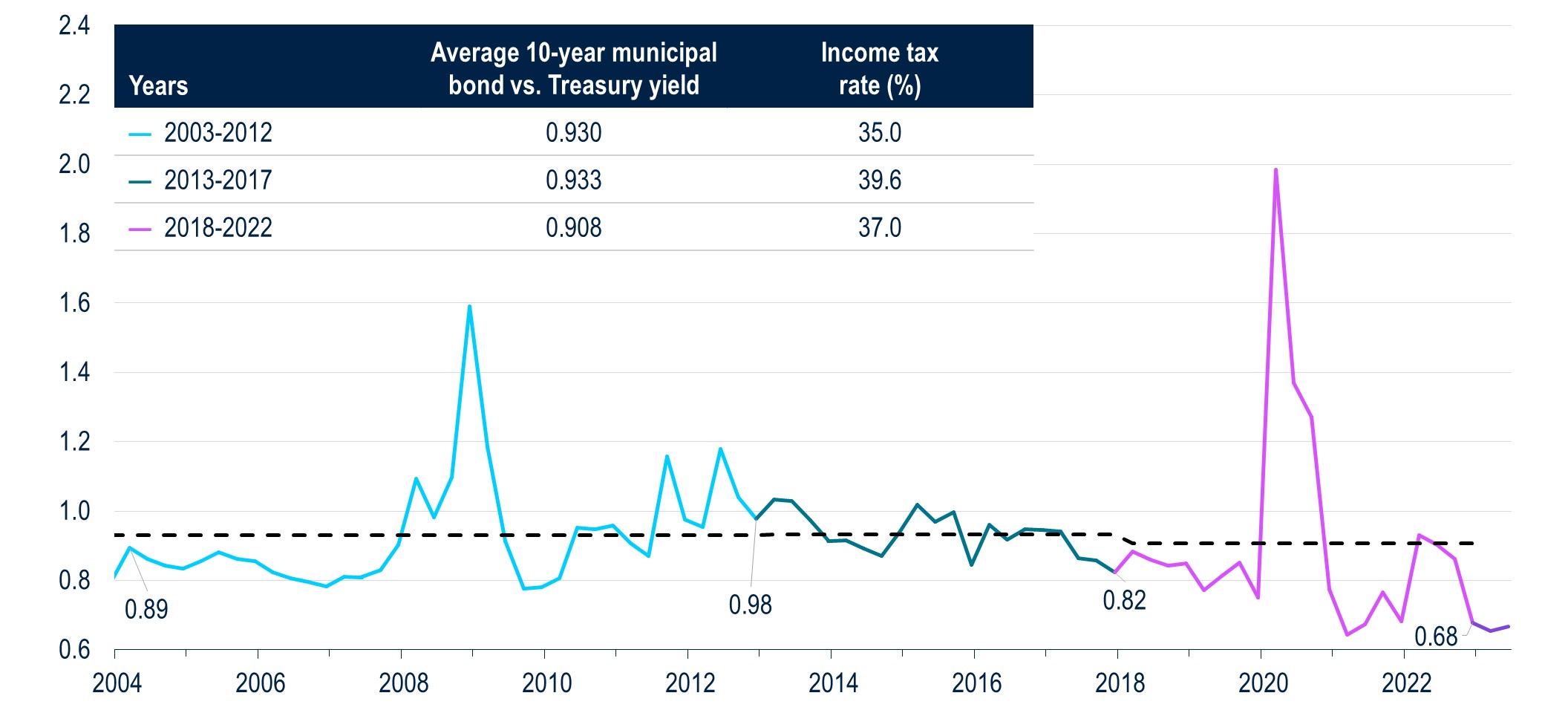

We also find that AAA municipal bond yields (which reflect the value of AAA states) can fluctuate in value relative to Treasury yields, even within the same tax rate regime (Figure 2).Figure 2: 10-Yr Muni v. Treasury Ratio

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in